The European market potential for sweet potatoes

The European sweet potato market has not yet reached its full potential. Growing import together with local production initiatives are fostering mainstream consumption and product development. Consumption is most developed in the UK. The Netherlands positions itself as a trade hub for northern European growth markets such as Germany and France.

Contents of this page

1. Product description

The sweet potato (Scientific name: Ipomoea batatas) is a root vegetable. Despite its name, the sweet potato does not belong to the same family as the potato (Solanum tuberosum). There are several kinds of sweet potato with different-coloured skin and flesh:

- Orange skin with orange flesh

- Red skin with orange flesh

- Yellow skin with white flesh

- Purple skin with white flesh

- Purple skin with purple flesh

The orange flesh varieties are most common in Europe, in particular the American Covington and the Spanish Beauregard. Other orange flesh types such as the Orleans and Evangeline are also being marketed. The white sweet potato variety remains more common in the ethnic market, and the purple varieties are a very small niche.

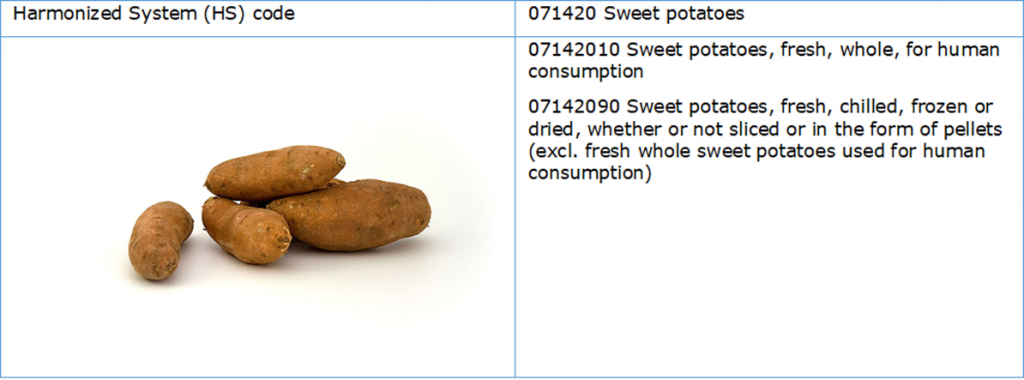

The statistics below focus mainly on HS 071420, which includes a small volume of frozen/dried sweet potatoes and pellets (for feed).

Table 1: Harmonised System (HS) code and Combined Nomenclature (CN) commodity codes for sweet potatoes

Source: Petr Kratochvil, Attribution, via Wikimedia Commons

{kind=link}

2. What makes Europe an interesting market for sweet potato?

The European import of sweet potatoes continues to grow. Product promotion and diversification will keep the demand strong in the years to come. However, in the next few years, increasing production costs may affect the enthusiasm of producers.

Short term: cautious market due to rising costs

The demand for sweet potatoes remains strong, but the market has become more cautious in 2021/2022. Suppliers fear that demand may slow down due to price inflation. Production already saw a great increase in cost. High costs and inflation in Europe may slow down market growth, but can also prove to be an opportunity for specialised growers.

Getting a good return on investment for sweet potatoes has become challenging. Sweet potatoes are cultivated in open fields, where farmers today prefer to grow more profitable crops such as cereal grains. In the next one to three years it will become clear what effect the expensive agricultural inputs, transport and packaging will have on the availability of sweet potatoes.

When production declines, there will be room for suppliers who know how to produce efficiently and ship cheaply. This will be a good moment to establish yourself as a specialised producer.

Long term: the demand for sweet potatoes will continue to grow

The European market for sweet potatoes has increased significantly in the past years and will continue to grow in the long term. There is a strong demand for imported sweet potatoes, which is why Europe is an interesting export market for foreign suppliers.

A year-round demand and the steady import from outside Europe provide opportunities for producers in a number of regions, including Northern Africa and the Americas. The import share is just over 60% of the total trade value (including European supply and re-export). Developing countries such as Egypt, China, South Africa and Honduras play a relevant role in the supply. A stronger demand will inevitably result in more import.

The total volume that was imported and traded between European countries in 2021 was an estimated 590,000 tonnes with a value of €478 million. The trade value increased by 53% over the last five years, and the import from developing countries by 161%. Roughly 90-92% of this volume concerns whole sweet potatoes for fresh human consumption. This makes fresh sweet potatoes one of the fastest growing products in the vegetable category in Europe.

Positive impulse from product promotion and diversification

Sweet potatoes have become a popular new food in Europe and a welcome addition to the consumption of other starchy food and root vegetables. Product promotion and diversification will further boost the demand for sweet potatoes.

Strong marketing efforts, in particular from American organisations such as the American Sweet Potato Marketing Institute (ASPMI), have placed sweet potato on the map in Europe. Since then, the increasing use of sweet potatoes by restaurants and developers of convenient products have added to the promotion of the product.

There is a growing effort in the food industry to transform sweet potatoes into baby food, crisps, fries, soups or prepared meals. Product development is especially strong in northern Europe. As a result, consumers are becoming more familiar with the product and more open to using sweet potatoes in their own kitchen.

Figure 2: Examples of developed products with sweet potato

| Private label sweet potato fries, sold by Coop supermarket | Sweet potato crisps in Edeka supermarket in Germany | Plant-based sweet potato katsu curry, sold by ASDA in the UK | Baby food with sweet potato |

|

|

|

|

| Photo by date-limite-app per Open Food Facts | Photo by kiliweb per Open Food Facts | Photo by kiliweb per Open Food Facts | Photo by and openfoodfacts-contributors per Open Food Facts |

Tip:

- Stay informed about the latest updates in the European sweet potato market through news items on Freshplaza and their regular overview of the global sweet potato market, Eurofruit, FreshFruitPortal, or FruiTrop.

3. Which European countries offer most opportunities for sweet potato?

The main import markets for sweet potatoes can be found in northern Europe, and include the United Kingdom, Germany, France and Belgium. The Netherlands is the main point of entry for other European markets. In larger markets, you can also find opportunities for organic sweet potatoes. Smaller markets in southern and eastern Europe show the fastest growth, but much of their supply is indirect.

Table 2: Main European importers and sweet potato origins, in 1,000 euro

| Highest import value overall | Important growth markets (2017-2021), according to size | Highest import value from non-European countries | Highest import value from developing countries | ||||

| Netherlands | 146,691 | Netherlands | 109% | Netherlands | 116,036 | Netherlands | 47,319 |

| United Kingdom | 105,542 | Spain | 461% | United Kingdom | 87,061 | United Kingdom | 41,837 |

| Germany | 51,034 | Poland | 199% | Germany | 30,267 | Germany | 12,259 |

| France | 47,831 | Italy | 130% | France | 21,484 | France | 10,084 |

| Belgium | 34,561 | Hungary | 178% | Spain | 5,543 | Spain | 3,360 |

| Spain | 11,133 | Czech Republic | 155% | Switzerland | 4,968 | Belgium | 2,568 |

Source: ITC Trademap

United Kingdom: A mature market with opportunities in new varieties and processing

The United Kingdom is the biggest consumer market in Europe for sweet potatoes. It has a well-developed processing industry and a taste for new products and cuisines. Sweet potatoes are consumed year-round in the UK and have become a valued addition to the consumption of conventional potatoes.

British people are among the biggest consumers of conventional potatoes in Europe and the largest consumers of frozen potatoes (mainly chips/fries). According to the UK’s Potato Processors’ Association the market share of processed potatoes is 71%. Sweet potatoes represent 5.5% of the standard potato market.

In 2021, a total of 129,400 tonnes of fresh whole sweet potatoes were imported. Another 29,700 tonnes of other products entered the country, such as freshly-cut and frozen sweet potatoes. This latter category is much smaller, but has grown faster by 60% over the past five years. With a limited export, domestic consumption is around 150,000 tonnes.

The consumption volume and growing import of pre-processed sweet potatoes show that the United Kingdom is a mature market. Some of the future growth must be expected within the processing industry such as baby food, frozen fries, crisps and ready-made meals. Part of the processing is outsourced, mainly to factories in China. Market maturity also offers opportunities for new varieties.

The United States and Egypt remain the biggest non-European suppliers of whole fresh sweet potatoes. The United States has been the preferred supplier for fresh sweet potatoes thanks to their close trade relation and promotional efforts, but Egypt is taking over a growing share with volumes increasing from 6,500 tonnes in 2017 to 25,400 tonnes in 2021. South Africa is also gaining market share with a volume of 6,000 tonnes in 2021. After Brexit (Britain leaving the EU), there may be less preference for EU supply, so competition from Egypt and other nearby countries could increase.

Tip:

- Find buyers of sweet potatoes in the trader search function of UK Trade Info. Use the commodity (HS) code 071420.

Netherlands: more than 80% re-export

The Netherlands has surpassed the UK in sweet potato import. The consumption per capita is likely almost as high as in the UK, but more importantly, the Netherlands offers an established trade route for sweet potatoes into Europe.

After the UK, the Netherlands was one of the first countries to adopt sweet potatoes as a regular root vegetable in their main fresh segment. Therefore, the domestic market is relatively well developed. Still, over 80% of the supply is re-exported, and the recent import growth is mainly attributed to the European markets that are supplied through the Netherlands. Because of this re-export, competitive pricing can be more important than the origin of the product.

The Dutch import of sweet potatoes has increased significantly from less than 100,000 tonnes in 2017 to 185,000 tonnes in 2021. With €116 million in 2021, it also has the highest import value from non-European suppliers.

There are several traders dealing with sweet potatoes, some of which can be found among the members of the Fresh Produce Centre. The presence of traders and a high service level of logistical suppliers gives the country a relevant role in the European sweet potato trade. As long as sweet potatoes are still a minor category or an exotic vegetable for many European consumers, Dutch traders will have no problem in maintaining a dominant trade position.

Tip:

- Use the Netherlands as a trade hub if you are struggling to enter European markets. There are several experienced companies with commercial networks throughout Europe, some of which can be found among the members of the Fresh Produce Centre.

Germany: Strong potential despite local preference

Germany offers strong potential for sweet potatoes. While consumers are still getting used to the new root vegetable, the market continues to expand.

Food media and supermarkets have a positive influence on the upward trend of sweet potato consumption. Supermarket chains such as Edeka share recipes with consumers and Rewe provides extensive information on the nutrition and preparation of sweet potatoes.

Orange-fleshed sweet potatoes such as the orange Beauregard and Bellevue variety are still the most popular, while consumption of white and purple varieties is less common among consumers. Fresh and frozen sweet potato fries are also popular products. According to Fruitnet, Edeka was the first German retailer to expand its segment beginning in 2016, with frozen sweet potato fries under a private label.

The German sweet potato import was worth €51 million in 2021. It is slightly less than in 2020, but 60% came directly from non-European suppliers. The United States and Dutch re-exports are the main sources. A significant share of the volume (up to 25%) concerned fresh and frozen fries and other processed products, mainly from China, the Netherlands and Belgium.

Consumers in Germany are paying more and more attention to origin, with a preference for German products if available. Several German growers, including organic farms, have started to cultivate sweet potatoes. The Federal Agency for Agriculture and Food (BLE) estimated that the German production in 2020 reflected between 9% and 14% of the available market volume, which is around 3,000 to 5,000 tonnes. However, German producers have much higher costs than their foreign competitors.

In the near future, you can expect the German market to expand further. There is enough potential for multiple origins, but also with an increasing preference for local or regional sources.

Tip:

- Activate the “Translation” function of your browser to make foreign websites available in your own language or change it to an English version.

France: Important market which depends on foreign sources

Sweet potatoes do well in the gastronomic trends in France. In consumption and total import volume, it is one of the largest markets in Europe with diversified sources.

France has had a growing import of sweet potatoes, but this stagnated after 2019. The import (and consumption) in recent years has been lower than expected due to the COVID-19 pandemic and the closure of restaurants throughout the country. An estimated 25-30% of the sweet potato market depends on these restaurants.

According to professionals in FruiTrop magazine, orange flesh potato varieties such as Beauregard, Orléans, Covington, Jewell, Georgia Jet and Evangeline represent more than 90% of French consumption. Medium and large sizes are most popular. White and purple varieties are niche products and mostly destined for the ethnic market. More than 90% of the sweet potato trade consists of fresh, whole roots. France seems less interested in prepared sweet potato products.

The largest part of the supply comes from parts of Europe such as Spain and Portugal. The United States and Egypt are the main non-European suppliers.

French farmers are also gradually developing domestic production of sweet potatoes. But the sweet potato production in France is still considered to be minor, and mainly consists of the orange-fleshed and license-free Beauregard variety. Even in the middle of the sweet potato season, from September to January, national production covers only 40% of the total supply. The domestic production is hardly competitive nor sufficient, so the country will keep depending on foreign sources.

Belgium: Potential in potato processing

Sweet potatoes fit well with the Belgian consumption and processing of common potatoes and are increasing in popularity. As a non-European exporter, you can target both importers and processors, but you will have to do your best to compete with farmers and suppliers in and around Belgium.

Belgium already has a high consumption of common potatoes, as well as a potato industry that produces potato fries. Belgium is home to Greenyard, one of the largest European companies in fresh and processed vegetables including sweet potatoes. There are at least 17 potato processors according to potato association Belgapom, all (potential) users of sweet potatoes. Sweet potato is a logical product to add to this existing industry. For example, Frito-Lay, a crisp-making division of Pepsico, has a factory in Belgium. Aviko, Ardo and FarmFrites, all producers of sweet potato fries, have facilities in Belgium as well.

Belgium imported 48,000 tonnes of sweet potatoes in 2021 with a value of €34.6 million. Based on trade statistics, the consumption of sweet potatoes (fresh and processed) has seen a strong growth from approximately 20,000 tonnes in 2017 to almost 40,000 tonnes in 2021. The import value from non-European sources is relatively low. Most sweet potatoes arrive via the Netherlands. There is also an increasing local production, for example by the growers of BelOrta. According to local news sources, the acreage went up from 100 hectares in 2019 to 260 hectares in 2021. This would suggest domestic production is heading towards 10,000 tonnes.

Spain: producer with growing imports

Spain is the largest sweet potato producer in Europe, with increasing imports. Currently the country finds itself among the fastest-growing markets.

Spain is one of the few countries in Europe with long-term experience in cultivating sweet potatoes (‘batata’ or ‘boniato’ in Spanish). It is home to the largest nursery in Europe, Vivero Santana, that supplies sweet potato plants. Spain’s sweet potato production is estimated to be around 50,000 or 60,000 tonnes, but there is no precise data. This production is expected to decline by 40% in 2022/2023, because of fierce competition, for example from Egypt. Spanish growers fear an overproduction and have seen prices go down in 2021 due to large volumes from different countries of origin. Meanwhile, the import continues to increase.

Spanish imports have increased from 2,000 tonnes in 2017 to 13,000 tonnes in 2021, with a value of over €11 million. Portuguese growers and Dutch traders are responsible for the largest share. But several other countries are also contributing to the growth. Among non-European suppliers are the United States, with surpluses from previous harvests, Argentina, Egypt, and a large number of smaller suppliers.

Spain will continue to play an important role in the sweet potato market as a producer, but also as an emerging import country. For non-European growers it can be interesting to find partnerships in Spain and combine their seasons to organise a year-round supply.

Tips:

- Stay ahead with high-quality production and sweet potato varieties. The production in Europe will increase and further improve, and as a foreign supplier you will need to operate at a similar level. When supplying maturing markets in northern Europe, select the varieties that are most suitable for processing.

4. Which trends offer opportunities or pose threats on the European sweet potato market?

The interest in new and healthy food products is a positive contributor to the success of sweet potatoes. Sweet potatoes have potential to cater to a diverse market. Diversification and mainstream consumption go hand in hand and will increase the number of varieties and uses.

Consumers are looking for new food experiences

European consumers are constantly exposed to cultural influences and ethnic diversity. Gastronomists and food marketeers use this diversity to tempt consumers to try new things. Consumer experience is an important success factor for sweet potatoes.

For European consumers, taste is of growing importance. The taste of sweet potato stands out from other tubers and potatoes and can be a unique selling point to the consumer.

Sweet potatoes are also a versatile product that is easy to integrate in the eating habits of consumers. It can be fried, cooked or mashed like potatoes, but also used in soups, salads, and even snack food and desserts. It is a vegetable that appeals to many consumers.

Although sweet potatoes are an easy root vegetable, it still requires education and inspiration to increase consumption. This is mainly a role for the marketeers of distributors and retailers in Europe, but as an exporter you could contribute as well with preparation tips and recipes.

Diversification helps sweet potato enter the mainstream market

The number of supply sources has increased and growers in Europe have started to produce sweet potatoes. The COVID-19 pandemic also triggered a stronger preference for local produce. More competition is not necessarily a bad thing. The market is on its way to becoming mature, which creates room for a year-round supply and the introduction of new varieties.

In a mature market, there is more potential for different sweet potato cultivars, including white and purple fleshed varieties. Before, the market was dominated mainly by Covington and Beauregard, two orange-fleshed varieties that covered 95% of the market. Now there are more and more varieties. Breeding companies such as NativaLand in Portugal support farmers in increasing the productivity, quality and diversity of their sweet potato crops, giving them access to some of the best licensed sweet potato varieties.

More focused on developing countries is the sweet potato agri-food systems programme of the International Potato Center (CIP). They are introducing biofortified, vitamin A-rich varieties in Africa and Asia, which are helping to improve nutrition. These global efforts will boost production as well as the future supply from developing countries.

The local production and varietal development are a sign that sweet potatoes have entered mainstream markets. At the same time, it will raise the product standards. As a foreign producer or exporter, you will need to keep up with the quality and innovation that takes place globally.

Attention to health and organic food

Consumers in Europe are becoming more aware of health issues and are paying more attention to their diet. This trend has had a positive impact on the marketing of sweet potatoes. Orange-fleshed sweet potatoes are the most popular variety in Europe. They are high in vitamins A and C, beta-carotene and fibres, and are often considered to be a healthier alternative to regular potatoes.

Thanks to the increased attention for health and environment, there is also a growing interest in organically produced sweet potatoes. The organic supply is increasing, but the volume and export quality are volatile. The organic cultivation of sweet potatoes comes with a number of difficulties, such as the availability of suitable organic fertilisers and weed control.

You can find organic sweet potatoes in mainstream supermarkets in Europe, for example at Tesco and Ocado in the UK, or at Ekoplaza, PLUS and AH in the Netherlands. The Egyptian company ITC has successfully capitalised on this trend by including certified organic growers in its portfolio and supplying specialised brands such as Nature & More by Eosta. With organic produce, consumers expect a sustainable product. As a supplier, you must have a transparent supply chain. Sustainable packaging and laser labelling are also strong aspects in the demand for organic.

Figure 4: Example of laser labelling of organic sweet potato in a German supermarket

Source: Photo by ICI Business

Tips:

- Verify with your buyer the possibilities for supplying organic sweet potatoes. The organic market is often an expertise of specific buyers that follow strict guidelines. Read more about the principles of organic agriculture on the website of IFOAM Organics International.

- Use varieties that fit the expectations of specific users or consumers. You can focus on the varieties that are sold most often or distinguish yourself by supplying other varieties that are superior in quality and taste or best used for processing.

- Read more about which trends offer opportunities on the European fresh fruit and vegetable market on the CBI market intelligence platform.

This study was carried out on behalf of CBI by ICI Business.

Please review our market information disclaimer.

Search

Enter search terms to find market research