The Polish market potential for coffee

Poland is the largest green coffee importer in Eastern Europe and the ninth-largest in Europe. Poland has a sizeable coffee roasting industry and ranked as the fifth-largest roasted coffee exporter of Europe in 2021. Certification still plays a relatively small role on the Polish coffee market, although demand is growing, mainly driven by the presence of international retailers and traders. Although Poland has been a traditional market for instant coffee, the specialty coffee market is maturing, providing interesting opportunities for exporters in this market segment.

Contents of this page

1. Product description

Harmonised System (HS) codes are used to classify products and to calculate international trade statistics, such as imports and exports. The focus of this study is green coffee beans, classified under HS code 090111 (coffee, not roasted, not decaffeinated). The available data do not distinguish between bulk, high-quality or specialty coffees. Coffee is consumed in Europe mainly as a beverage with multiple preparations. However, its extract is also used in the production of coffee-flavoured products like pastries and liqueur.

Approximately 124 coffee species exist in the wild, of which only a few are commercially relevant. The two most important species on the market are:

- Coffea Arabica (Arabica): Referred to as a highland coffee, because it grows best at altitudes between 600 and 2,000 metres, Arabica is the most dominant species in the coffee market, representing about 75% of global coffee production. Each coffee tree yields an average of two to four kilos of cherries. Arabica beans are fairly flat and elongated. Arabica coffee beans have a smoother, more aromatic and more flavourful taste compared to Robusta. Arabica beans have a caffeine content of approximately 1.5%. Due to its characteristics, Arabica beans make up the largest share of specialty coffees in Europe.

The main sub-varieties of Arabica are the Yemen accession, which is subdivided into the Typica and Bourbon coffee lineages, and the Ethiopia/Sudan accession. Examples of the Ethiopian and Sudanese cultivars are Geisha, Java, Sudan Rume and Tafari Kela.

Examples of Typica cultivars are the Hawaiian Kona, Jamaican Blue Mountain, SL14 and Maragogipe. Examples of the Bourbon cultivars that are grown mostly in Latin America are Caturra, Villa Sarchi and Pacas. Examples of Bourbon cultivars grown in East Africa are Jackson, K7, SL28 and SL34.

- Coffea Canephora (Robusta): Robusta coffee can be considered a lowland coffee, as it grows best at altitudes below 600 metres. Robusta accounts for around 20% of global coffee production. Its beans have a caffeine content of approximately 2.7%. Robusta is less susceptible to pests and diseases than Arabica. Its beans are smaller and rounder than Arabica beans. When roasted, Robusta beans generally have a stronger and harsher taste than Arabica, which is often described as bitter. Robusta beans are often used in coffee blends and are commonly used for instant coffee production.

Examples of crossbreeds of the Arabica and Robusta species are Catimor, Castillo (the most commonly grown coffee plant in Colombia), IHCAFE90, Ruiru 11, Sarchimor and Obatá.

2. What makes Poland an interesting market for coffee?

Compared to West European countries, Poland is a relatively small green coffee importer. But the country is Eastern Europe’s largest importer. Green coffee imports have been increasing steadily, with growing direct imports from producing countries. Poland is also home to a large coffee-roasting industry.

Poland is the largest green coffee importer of Eastern Europe

Poland ranked as Europe’s ninth-largest green coffee importer in 2021, and the largest importer in Eastern Europe. According to data from Eurostat, Poland imported 3.6% of all European green coffee in 2021, amounting to 128 thousand tonnes. Polish imports saw an average year-to-year growth of 2.4% between 2017 and 2021.

About 25% of total Polish green coffee imports were sourced directly from producing countries, amounting to 32 thousand tonnes in 2021. Between 2017 and 2021, direct imports grew at an average annual rate of 7.0% in volume. The largest coffee-producing suppliers to Poland were Brazil and Vietnam, accounting for more than 80% of total direct coffee imports. In 2021, about 68% of total Polish coffee imports came from Germany, which is an important trade hub to all Eastern Europe.

Coffee imports mainly enter Poland via the ports of Gdynia, Gdańsk and Szczecin.

Poland is the fifth-largest roasted coffee exporter of Europe

Only 1.1% of Polish coffee imports in 2021 were re-exported, mainly to other Eastern European countries like Ukraine and Slovakia. The fact that most of the green coffee stays within the country indicates that Poland has a relatively big and important coffee-roasting industry. Poland ranked as the tenth-largest roasted coffee industry in the EU in 2021. Production volumes amounted to 38 thousand tonnes in 2020, accounting for 2.1% of total EU volumes. Between 2016 and 2020, roasted coffee production in Poland increased at an average annual rate of 2.6%.

Poland exported 64 thousand tonnes of roasted coffee in 2021. This makes Poland the fifth-largest roasted coffee exporter of Europe, with 5.7% of total exports. Larger roasted coffee exporters were Italy (25% share of export market), Germany (23%), Switzerland (9.6%) and the Netherlands (9.5%). The main destination markets of Polish roasted coffee were Ukraine (19% of Polish roasted coffee exports), Germany (15%), the Netherlands (14%) and Czech Republic (12%).

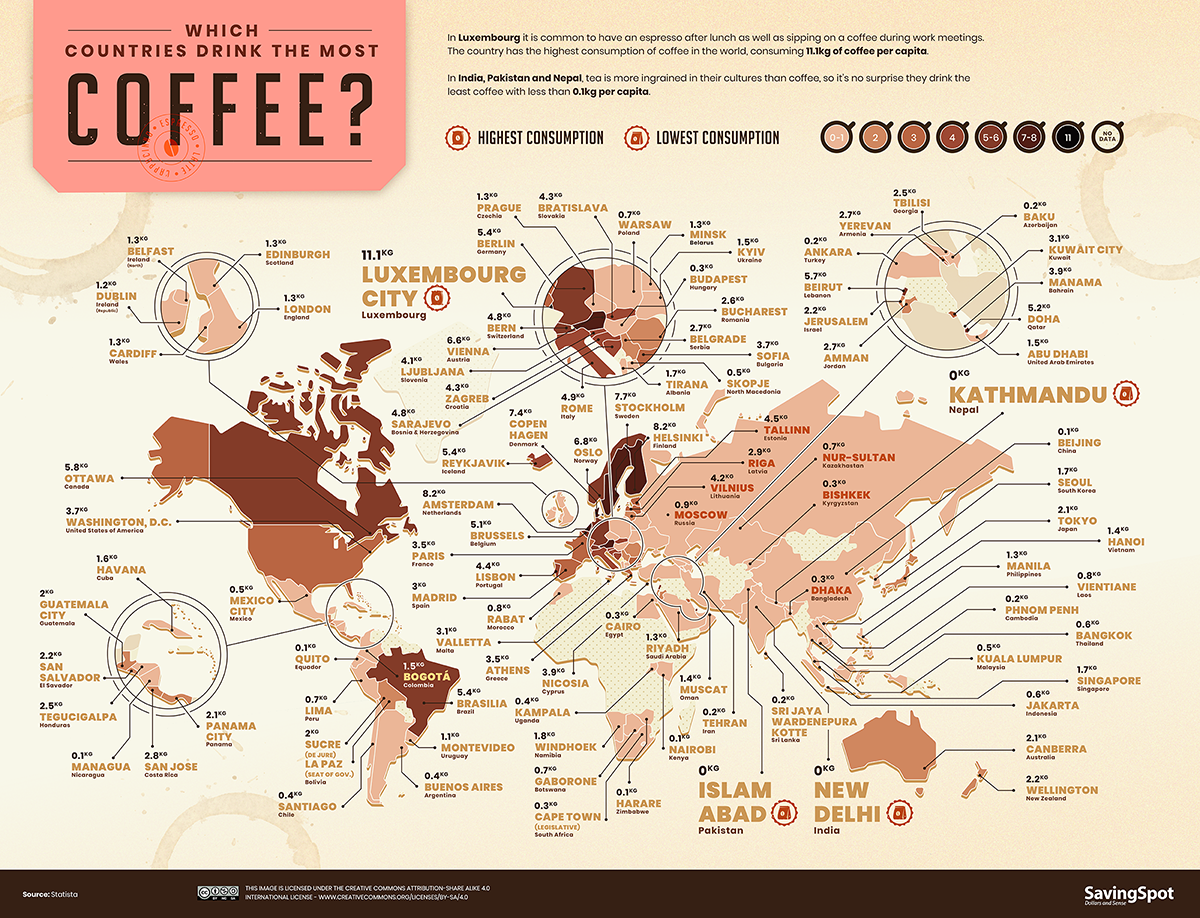

Regarding consumption, more than 80% of adults in Poland consume coffee every day. Instant coffee still takes up the largest share of consumption. Annual coffee consumption per capita in Poland is low and it is estimated to be between 0.7 kg and 2.5 kg, well below the 5 kg average in Europe.

{kind=link}

Tips:

- Activate the “Translation” function of your browser to make the studies available in your native language.

- Access EU Access2Markets to analyse Polish trade dynamics yourself and to determine your export strategy. By selecting a specific country as your reporting country, you will be able to follow developments such as trade flows with established suppliers, the emergence of new suppliers and changing patterns in direct and indirect imports.

- Refer to the ITC Coffee Guide – 4th Edition. This guide contains lots of information, also about the practical aspects of coffee trade. Check the content table to see what you want to learn about.

- See our Polish Market Entry study to find a list of industry players active on the Polish market.

- See our study of trade statistics for coffee for more detailed information about the European trade in green coffee beans.

3. Which trends offer opportunities on the Polish market?

The market size of certified and specialty coffee in Poland is relatively small compared to other European coffee markets, especially in Western Europe. But the interest in certified and specialty coffees is growing among Polish consumers, providing interesting opportunities for exporters in these market segments.

Poland is a market with high potential for certified coffees

Poland is a small market for certified coffees, but it shows positive growth prospects. This is driven in large part by the dominance of large multinational retailers and roasters in the country. These industry actors have made sizable sustainability commitments, often including certification efforts. In fact, more and more multinational retailers are starting to commit to only sourcing certified coffee.

For Fairtrade certification, availability, visibility and recognisability on the Polish market has grown and resulted in increased sales. According to a Fairtrade Poland review, Polish retail sales of Fairtrade products reached €119 million in 2020, over three times as much as in 2018. Coffee products made up 14% of the sales in 2020. Fairtrade research in 2021 concluded that Polish consumers most commonly associate the Fairtrade mark with coffee.

The leading retail channel for Fairtrade coffee in Poland is ORLEN, the country’s largest petrol station chain. ORLEN has been selling Fairtrade-certified coffees since 2008. Also, the multinational retailer Lidl (Germany) has a presence in Poland, with an offer of Fairtrade-certified coffee products. Fairtrade Poland provides an overview of shops, gas station chains, roasters and online channels where consumers can buy Fairtrade coffee, as well as coffee brands and products that are Fairtrade-certified.

Rainforest Alliance products are also available in Poland, mainly through multinational roasters and traders. For instance, German roaster Tchibo sells Rainforest Alliance/UTZ-certified (as well as Fairtrade-certified) coffees in Poland. Coffee shops like Cafe Sati Polska and Tommy Cafe sell Rainforest Alliance-certified coffee in Poland. Bero Polska is an example of a Polish trader buying all sorts of certified coffees.

Small but growing organic market in Poland

Poland is the largest organic market in Eastern Europe, where countries generally have small markets for organic products at less than 2% of total food sales. According to the FiBL retail sales database, Poland’s organic retail share reached 0.6% in 2019. In Poland, retail sales reached €314 million that same year. This was a year-to-year growth of 17% since 2015. Consumer spending on organic products is growing fast and has grown even faster during the pandemic as consumer interest in healthier food options grew. In the first half of 2020, the organic products market grew by 28% compared to the same period in 2019. Between 2018 and 2019 this figure was 20%.

At the same time, consumer demand for organic coffee in Poland lags behind consumption of other organic products. While consumers often buy organic fruits, vegetables, and eggs, around 10% of Polish consumers regularly buys organic coffee or tea (once a week or month). Over 60% of consumers in Poland never buys organic coffee.

Increasing interest in specialty coffee in Poland

Despite the large market for instant coffee in Poland, there is a growing demand for high-quality and specialty coffees. This trend has been further driven by the COVID-19 pandemic and related lockdowns.

As at-home-consumption increased to 63% in 2020 compared to 57% in 2019, sales of specialty beans and espresso coffee machines soared. Compared to 2020, sales of coffee beans increased by 21% in 2021. From January to November 2020, the espresso machine market increased 17% compared to the same period in 2019, reaching over €194 million. The total coffee machine market was worth €116 million in the first half of 2021, making Poland the third market for coffee machines in Europe.

The growing number of specialty coffee shops and micro roasters in Poland also illustrates a consumer interest in adding quality and variety to their coffee. Currently, Poland houses 183 coffee shops and roasters, while the first shops opened in 2010. Examples of specialty roasters and shops include Karma Roastery, Typika, and Wesoła Cafe.

As the specialty niche market starts to flourish, Poland has joined the Specialty Coffee Association (SCA) with a national chapter. Moreover, in 2019 the first SCA-certified campus in Eastern Europe, called Raf&Co, opened in Warsaw, Poland. The Raf&Co Coffee Campus is approved to teach all SCA modules, certify and train individuals for the Q-Grader License.

The growing number of specialty roasters and shops and the growing interest in high-quality coffees bring new opportunities for exporters of specialty coffees, for example in new direct trade relations. However, specialty coffee is still a niche market in Poland. The specialty coffee market accounts for less than 2% of the country’s entire coffee market.

Tips:

- See our study on trends in coffee to learn more about current trends in the European market.

- See the Specialty Coffee Association’s national chapter Poland for more information about the Polish specialty coffee market.

- Refer to the website of the Research Institute of Organic Agriculture (FiBL) Statistics to access data about the organic markets in Europe and the world.

- Learn more about global organic developments in the report The World of Organic Agriculture: Statistics and Emerging Trends 2022. You can download the PDF document here.

- Check the website of Fairtrade Poland for a list of companies manufacturing and distributing Fairtrade certified products.

- Before engaging in a certification programme, make sure to check that a label has sufficient demand in your target market and whether it will be cost-beneficial for your product, always in consultation with your potential buyer.

- See our study on doing business with European coffee buyers for more tips on marketing and promoting coffee.

- Find potential business partners in Poland by checking the customer database of Fairtrade-certified operators such as traders, manufacturers and/or processors), Rainforest Alliance-UTZ certified coffee supply chain actors and Polish organic coffee importers.

- Are you interested in exporting high-quality coffee? Learn more about cupping scores on the website of the Specialty Coffee Association (SCA). You can also consider getting a Q-grader certificate to be able to cup and score your Arabica coffee according to international standards. If you produce or export Robusta coffees, it is also possible to become an R-grader.

Gustavo Ferro and Lisanne Groothuis of ProFound – Advisers In Development carried out this study on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research