Entering the Polish coffee market

Although the share of direct imports of green coffee into Poland is increasing, Germany is still its biggest supplier. The market is dominated by multinational roasters and coffee brands, though the specialty coffee scene is growing. Given the presence of large multinationals in the market, minimal certification requirements such as Rainforest Alliance are gaining importance.

Contents of this page

1. What requirements and certification must coffee comply with to be allowed on the Polish market?

You can only export coffee to Poland if you comply with strict European Union (EU) requirements. Buyer requirements can be divided into:

- Mandatory requirements

- Additional requirements that buyers often have

- Requirements for niche markets

The highlights for these requirements are given below, specified for the Polish market where relevant.

Legal and non-legal requirements you must comply with

Legal requirements

You must follow the European Union legal requirements applicable to coffee. These rules mainly deal with food safety, where traceability and hygiene are the most important themes. Special attention should be given to specific sources of contamination, namely:

- Pesticides – consult the EU pesticide database for an overview of the maximum residue levels (MRLs) for each pesticide.

- Mycotoxins/mould, particularly Ochratoxin-A (OTA) – although no maximum OTA limits have been set for green coffee, green coffees / origins with high OTA levels may be characterised as ‘high risk’.

- Mineral Oil Aromatic Hydrocarbons (MOAHs) – green coffee can get contaminated with MOAHs during all stages of the supply chain. Officially there are no maximum MOAH levels established in Europe yet.

Quality requirements

In general, to determine coffee quality the coffee undergoes both a physical evaluation of green and roasted coffee, as well as a sensory evaluation of the roasted coffee prepared as a drink.

Green coffee assessment

Green coffee is first graded and classified for quality before export. There is no universal grading and classification system for coffee. The Specialty Coffee Association’s standards for green coffee grading are often used as a point of reference. However, most producing countries have and use their own grading systems.

Grading and classification is usually based on the following criteria:

- Altitude and region

- Botanical variety

- Processing method – wet/washed, dry/natural, honey, pulped naturals

- Screen size (note: screen size is important to ensure uniform roasting which improves the quality of the final product)

- Number of defects or imperfections

- Bean density

- Cup quality

Buyers in Poland will also do a green coffee assessment. This includes a screen size evaluation, defect count, and an assessment of bean colour, appearance and smell. This is followed by a moisture check and water activity analysis. Sample roasting is then performed, to evaluate green coffee quality and uniformity.

Sensory assessment: coffee cupping

Coffee is assessed and scored by a method called cupping. Buyers will use different protocols and standards to conduct a sensory assessment. However, the SCA recommends specific guidelines and protocols for cupping coffee. The most widely used cupping tool is the SCA’s Coffee Taster's Flavor Wheel. Some quality attributes assessed are: flavour, fragrance/aroma, aftertaste, acidity, body, uniformity, balance, cleanliness, sweetness and off-notes.

Note that there is no exact definition of specialty coffee within the coffee industry. The Coffee Quality Institute and the Specialty Coffee Association consider that coffees graded and cupped with scores below 80 are considered standard quality and not specialty. Nevertheless, the exact minimum scores defining specialty coffee differ per country and per buyer. Some buyers consider 80 too low and demand a cupping score of 85 or higher.

If you sell specialty coffee, it is important for buyers to know the cupping score of your coffee. Although not mandatory, adding this information to the documentation of the coffee you are exporting might add value. It is very important to be aware of the quality of your coffees, either by inquiring with local cupping experts or becoming a cupping expert yourself.

Labelling requirements

Labels of green coffee exported to Poland should comply with the general food labelling requirements of the European Union. The label should be written in English and should include the following information to ensure traceability of individual batches:

- Product name

- International Coffee Organisation (ICO) identification code

- Country of origin

- Grade

- Net weight in kilograms

- For certified coffee: name and code of the inspection body and certification number

Figure 1: Example of green coffee labelling

Source: Escoffee

Packaging requirements

Green coffee beans are traditionally shipped in woven bags made from jute or hessian natural fibre. Jute bags are strong and robust. Other materials, such as Grainpro or other innovative material like Videplast liners, are often used to pack specialty coffees inside jute bags. These materials have added value over traditional packaging, as they preserve grain quality, avoid post-harvest loss, reduce solid waste, reduce farmer’s net carbon footprint, and facilitate chemical free storage.

Most green coffee beans of standard quality imported into Poland are packed in container-sized bulk flexi-bags that hold roughly 20 tonnes of green coffee beans each. The remaining green coffee is transported in traditional 60 kg jute sacks, each with a net volume of 17 tonnes to 19 tonnes of coffee. Although the 60 kg bag is the most common, some countries use bags holding 46 kg, 50 kg, 69 kg or 70 kg.

Other packaging used in transporting coffee includes polypropylene super sacks for 1 tonne of coffee, polyethylene liners for 21.6 tonnes and vacuum-packed coffee. These techniques provide two advantages in the coffee trade, namely increasing efficiency and maintaining or preserving quality.

Figure 2: Examples of coffee packing: jute bag, container-sized flexi bag, GrainPro and Videplast liner

Sources: raadtradingco.com, bls-bulk.com and GrainPro

Tips:

- Activate the ‘Translation’ function of your browser to make the studies available in your native language.

- For the full buyer requirements, read the CBI study on buyer requirements for coffee in Europe or consult the specific requirements for coffee on the European Commission’s website Access2Markets.

- Check EUR-Lex for more information on limits for different contaminants. For specific information on the prevention and reduction of Ochratoxin A contamination, refer to the FAO website. Use the search tool to find the Codes containing information on Ochratoxin A and select your preferred language.

- For information on safe storage and transport of coffee, refer to the website of the Transport Information Service.

- Read more about quality requirements for coffee on the website of the Coffee Quality Institute.

- Find out more about delivery and payment terms for your green coffee exports by reading our study Organising your coffee bean exports to Europe.

Additional requirements

Additional food safety requirements

Expect buyers in Poland to request extra food safety guarantees from you. Regarding production and handling processes, you should think of:

- Implementation of good agricultural practices (GAP): The main standard for good agricultural practices is GLOBALG.A.P., a voluntary standard for certification of agricultural production processes that provide safe and traceable products. Certification organisations, such as Rainforest Alliance/UTZ, often incorporate GAP in their standards.

- Implementation of good manufacturing practices (GMP): These general principles provide guidance on post-harvest processes such as washed or natural processing, manufacturing, testing and quality assurance to ensure that the product is safe for human consumption. Your GMP plan should include guidelines about at least your processing facility and equipment as well as your warehouse and transportation.

- Implementation of a quality management system (QMS): Buyers are increasingly requiring a system based on Hazard Analysis and Critical Control Points (HACCP) as a minimum standard for green coffee production, storage and handling. Regularly checking the residue levels in your green (and roasted) coffee is an example of a measure that could be included in this system. It is particularly important to check for (and aim to prevent) Ochratoxin-A (OTA), polyaromatic hydrocarbon (PAH) and pesticide contamination, such as glyphosate contamination. Proactively obtaining certificates of analysis on a regular basis for the coffee you produce and export is recommended, preferably from an EU-accredited laboratory such as Eurofins or Tüv. You may also decide to obtain ISO 9001 certification for your quality management system.

- For roasted coffee, HACCP might be required, and this must sometimes be accompanied by certification from the Global Food Safety Initiative (GFSI) such as BRC Global Standard Food Safety, FSSC 22000, IFS Food or SQF Institute. Read our study on coffee roasted at origin to find more information about specific requirements for roasted coffee.

Additional sustainability requirements

Corporate responsibility and sustainability are very important throughout the European coffee sector. Coffee industry players, especially the multinationals in Poland, have sustainability policies reflecting their relationship with farmers and transparency in their operations, as well as their social and environmental impact in the place of origin. Examples of these company policies or codes of conduct can be found on the website of Neumann Kaffee Gruppe, of which Polish importer Bero Polska is a part. Another example of a corporate sustainability scheme is Olam’s AtSource. This is a sustainability insights platform which helps customers to meet multiple social and environmental targets and guarantee traceability in agricultural supply chains.

As an exporter, adopting codes of conduct or sustainability policies related to your company’s environmental and social impact may give you a competitive advantage. In general, buyers will likely require you to comply with their code of conduct, and/or fill out supplier questionnaires regarding your sustainability practices.

Certification standards are very often part of the sustainability strategy of traders, coffee roasters and retailers. As such, a standard like Rainforest Alliance/UTZ has become increasingly important in the mainstream coffee market.

Apart from these sustainability requirements, it is important to be aware that the EU is implementing its so-called European Green Deal. This Green Deal is aimed at making Europe sustainable and climate neutral by 2050. To achieve this goal, the EU is working on legislation that requires companies to address human rights and environmental standards in their value chains, including those that trade in coffee. As with the corporate codes of conduct, companies will require you to comply with these additional requirements. The EU is also working on a European due diligence solution to stop EU-driven deforestation, which also pertains to coffee cultivation.

Tips:

- Refer to the International Trade Centre Standards Map or the Global Food Safety Initiative website to learn about the different food safety management systems, hygiene standards and certification schemes.

- Read CBI’s article on The EU Green Deal – How will it impact my business? to find out more about this regulation and how to comply with it.

- Have a written plan about your food safety control. Review and update your plan when changes occur in your business operations, or at least every couple of years.

- Find out which standards or certifications are preferred by potential buyers in your target segment. Buyers may have preferences for a certain food safety management system or sustainability label depending on their end clients and distribution channels.

- Carry out a self-assessment to measure how sustainable your production practices are. You can fill out this Excel form by the Sustainable Agriculture Initiative (SAI) Platform to assess your farm’s sustainability performance.

- See the list of Rainforest Alliance/UTZ registered coffee actors in Poland to identify interesting players. Learn which ones are certified to buy your Rainforest Alliance/UTZ certified coffee.

- See our study on certified coffee for more information about the demand on the European market, trends and specific trade channels.

Niche requirements

EU Organic

In order to market your coffee as organic in the European market, it must comply with the regulations of the European Union for organic production and labelling. Regulation (EC) 2018/848 lays down rules on organic production and labelling. Regulation (EC) 1235/2008 describes the implementing rules of the EU legislation for imports of organic products from third countries. Obtaining the EU organic label is the minimum legislative requirement for marketing organic coffee in the EU.

If you are new to organic, you must first go through a conversion period of organic farming before you can market your coffee as organic. This often takes at least three years and requires yearly inspections. To remain organic certified, you should continue to undergo a yearly inspection and audit by an accredited certifier. This is needed to ensure that you continue to comply with the rules on organic production. Refer to this list of recognised control bodies and control authorities issued by the EU to ensure that you always work with an officially recognised accredited certifier.

Note that all organic products imported into the EU must have the appropriate electronic Certificate of Inspection (COI). These COIs must be issued by control authorities prior to the departure of a shipment. This means you will have to obtain the necessary information, such as the importer’s address and TRACES number, first consignee and the seal and vessel number of your container. If this is not done, your product cannot be sold as organic in the European Union and will be sold as a conventional product. COIs can be completed by using the European Commission’s electronic Trade Control and Expert System (TRACES).

Fair trade

Before you can market your coffee as fair trade, an accredited certifier must audit your growing and processing facilities. The most common fair trade standard in Poland is Fairtrade, for which the accredited certifier is FLOCERT.

High-end specialty coffee

The high-end specialty coffee segment is characterised by high cupping scores (usually 84+), innovative processes (such as natural and honey processing), direct trade relations, and high transparency and traceability from source to consumer. This means that buyers of these coffees ask for requirements that go beyond the requirements for certification.

Besides high quality, these buyers are interested in your stories from origin; for instance about your coffee farm, the coffee growers and your processing facilities. This implies that you should know the specifics of your coffee, from soil management to the cup, from variety to processing, from external suppliers to farmers, and must be willing to share these honestly. Other than that, direct trade may result in more frequent coffee farm visits and product assessments by your buyers, as well as long-term business relations.

Tips:

- Learn more about organic farming and European organic guidelines on the European Commission website and the Organic Export Info website.

- Familiarise yourself with the range of organisations and initiatives that offer technical support to help you convert to organic farming. Start your search by learning about the organic movement in your own country and inquire about support programmes or existing initiatives. Refer to the database of affiliates of IFOAM Organics to search for organic organisations in your country.

- Find importers that specialise in organic products on the website Organic-bio.

- Try to visit trade fairs for organic products, like Biofach in Germany. Check out their website for a list of exhibitors, seminars and other events at this trade fair. There you will also find organic certification bodies on the exhibitors’ list.

- If you produce coffee according to a fair trade scheme, find a specialised Polish buyer that is familiar with sustainable or fair trade products, for instance via the FLOCERT customer database.

- Use this cost calculator to estimate what costs will be involved for your organisation to become Fairtrade-certified.

- Ask quotations from different certifiers before you decide with whom you want to work. Ask for timelines and an estimation of how many days will be charged.

- Try to combine audits in case you have more than one certification, to save time and money. Also investigate the possibilities for group certification with other producers and exporters in your region.

2. Through what channels can you get coffee on the Polish market?

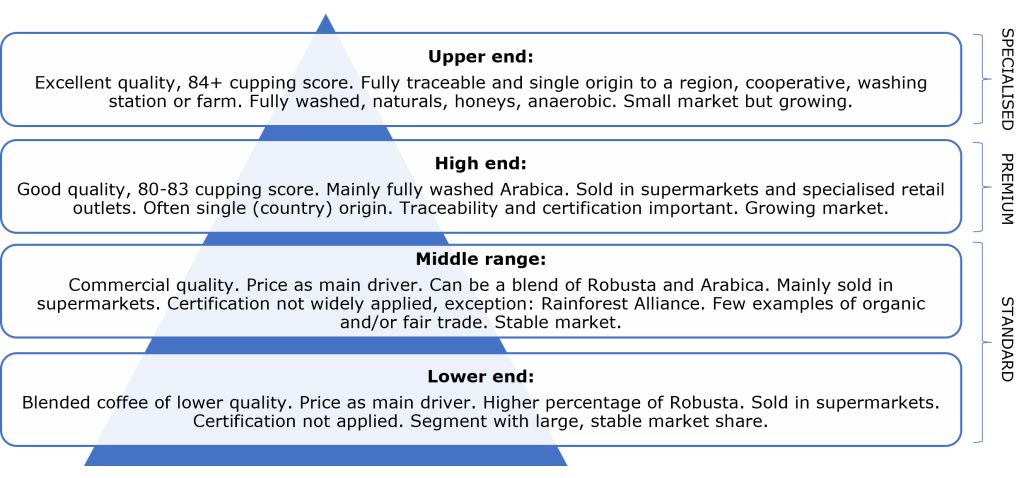

The Polish end market for coffee can be segmented by quality. The high-end and upper-end segments represent a small but growing niche market. Suppliers in producing countries mainly enter the Polish market through importers or medium-sized and large roasters.

How is the end market segmented?

The Polish coffee end market can be segmented as follows:

Figure 3: Coffee end market segmentation by quality

Source: ProFound

In Poland, supermarkets are the main sales channel for coffee. Supermarkets mainly sell standard quality coffee products, comprising the lower-end and middle-range segments. These segments also include a wide range of retailer’s own coffee products. These products are popular as they offer the same characteristics as branded products, but usually at more affordable prices. The total share of private label products in Polish retail reached over 31% in 2021. High-end products are increasingly for sale in supermarkets as well, although this market in Poland is only starting to develop.

The largest supermarkets in Poland are:

- Biedronka, owned by the Portuguese company Jerónimo Martins.

- Dino, owned by the Polish Grupo Dino.

- Kaufland, owned by the German Schwarz Gruppe – present in Bulgaria, Croatia, the Czech Republic, Poland, Romania and Slovakia.

- Lidl (also part of the Schwarz Gruppe) – with stores in Bulgaria, Romania, Croatia, Hungary, Poland, the Czech Republic, Slovakia and Slovenia.

- ABC-Supermarket, part of Eurocash Group.

- Zabka, part of CVC Capital Partners with stores in Poland and Czech Republic.

- lewiatan, part of Eurocash Group.

Low end: The coffees in the low-end segment are mainstream, low-quality and mainly blended coffees. These blends are characterised by high shares of Robusta beans. Besides some mainstream brands, the lower-quality private label products from supermarkets also belong to the low-end segment. In addition, most coffee pads and instant coffee belong to this low-end segment. Coffees at the low end of the market are mainly sold in supermarkets and through service channels, such as offices and hotels.

Product and price examples in the low-end segment, based on Auchan retail prices in 2022, include:

| Product | Image* | Price (€/kg) | |

| Low-end | Tchibo (ground coffee, uncertified, 500-gram package) |

| 5.68 |

| Jacobs (ground coffee, uncertified, 500-gram package) |

| 11.54 |

*Source of pictures: www.auchan.pl

Mid-range: Mid-range coffees are commercial coffees with a consistent quality profile. This segment typically consists of blends with a higher proportion of Arabica compared to coffees in the low-end segment. The mid-range segment represents a stable coffee market, in which Rainforest Alliance-certification is increasingly important.

Mid-range coffees are also most often sold in supermarkets and by the food service industry. Examples of mid-range products and prices, based on Auchan's retail prices in 2022, include:

| Product | Image* | Price (€/kg) | |

| Mid-range | Lavazza (whole beans, 100% Arabica, uncertified, 1-kilogram package) |

| 16.24 |

| Jacobs, Barista (whole beans, Rainforest Alliance-certified, 1-kilogram package) |

| 16.46 |

*Source of images: www.auchan.pl

High end: These are premium coffees of good quality, and mainly consist of Arabicas. These coffees are often single origin, tracing back to the country level. Story telling is important in this segment, especially for branding and marketing purposes. Usually, these premium coffees have packages where the origins of the product are explicitly stated, as well as other features that represent an added value for the product, such as social/environmental impact. Certification is also important. Most coffees will be certified according to Fairtrade, organic and/or other certification standards. Within Europe this high-end segment is fully integrated in supermarkets, although in Poland this is still a relatively small market.

Examples of high-end products and prices, based on Auchan's retail prices in 2022, include:

| Product | Image* | Price (€/kg) | |

| High-end | Real Coffee Roaster (whole beans, blend from pulped natural from Brazil (Cerrado) and washed from Colombia (Medellín), uncertified, 250-gram package) |

| 23.34 |

| Woseba (whole beans, organic-certified, 500-gram package) |

| 23.93 |

*Source of images: https://www.auchan.pl

Upper end: The upper-end segment consists of specialty coffees of excellent quality, often from micro or nano-lots that undergo processing methods such as naturals and honeys. These are fully traceable and single origin beans that trace back to cooperatives, washing stations or estates. Cupping score is 84 and above.

Sustainability certifications are not common in this segment, except for organic. This is because sustainability practices are often commonplace among buyers. Long-term contracts between suppliers and buyers characterise the upper-end segment, as well as higher prices.

Coffees in this segment are mainly sold directly by specialty roasters, at their physical and web shops as well as at coffee events. An example of a coffee event is the Warsaw Coffee Festival. Examples of specialised Polish coffee web shops are kawa.pl and Coffeedesk. For examples of Polish specialty roasters and cafés, see the website European Coffee Trip.

Examples of coffees in the high and upper-end market segments include (prices from 2022):

| Product | Image* | Price (€/kg) | |

| Upper-end | Variety: Red Bourbon Process: Natural |

| 47.03 |

Variety: Ethiosar Process: Natural |

| 54.73 |

*Source of images: Java Coffee Roasters and Coffee and Sons

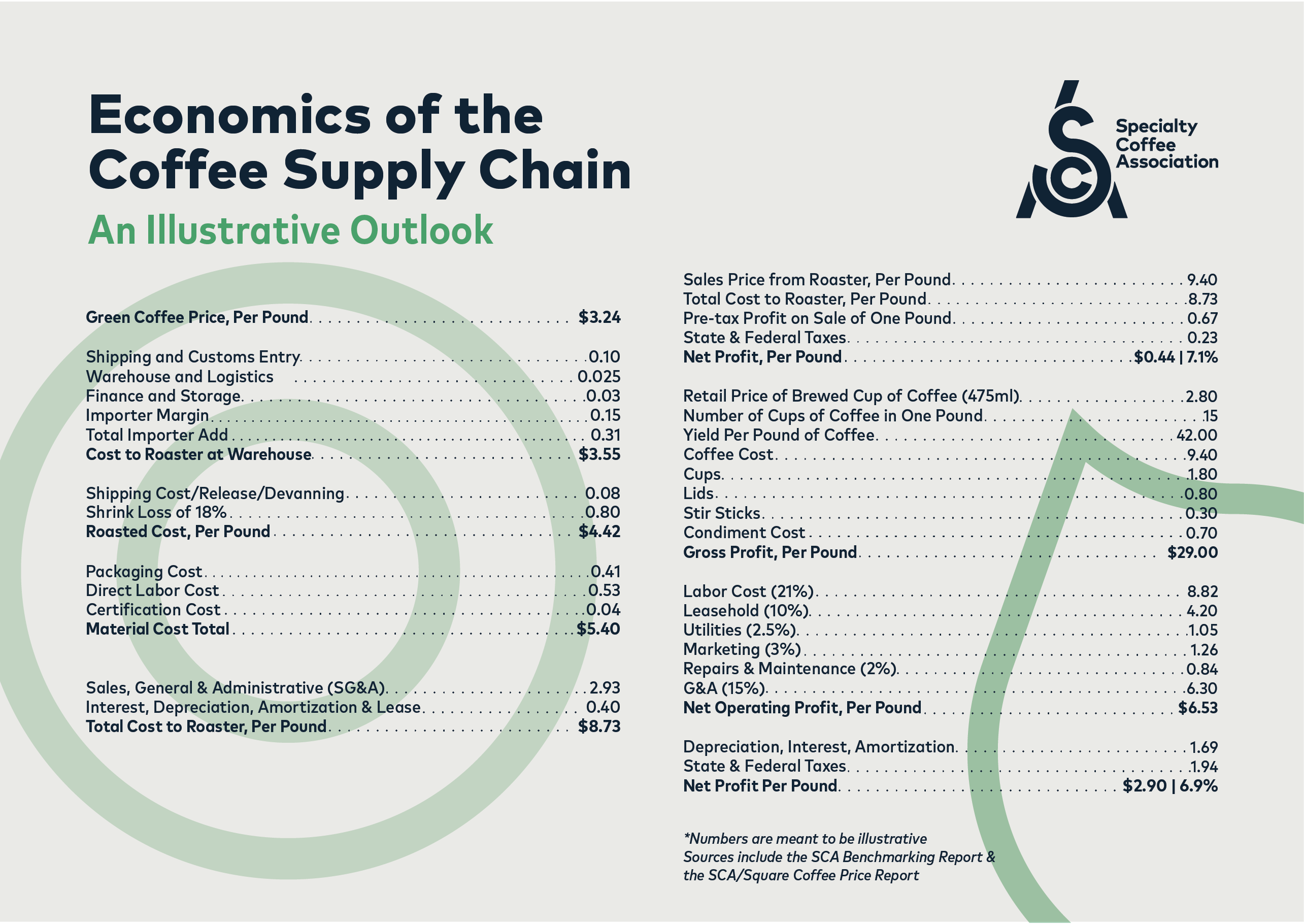

Value distribution: As shown by the above examples, end-market prices for coffee vary depending on the targeted market segment. Green coffee export prices typically amount to only 5% to 25% of the end-market prices, depending on the coffee quality, the size of the lot and the supplier’s relationship with the buyer. Figure 4 below shows the value distribution of wholesale mainstream coffee (standard quality). Roasters often end up taking more than 80% of the wholesale coffee price. A coffee farmer takes about 10%.

Value distribution for specialty coffees in the high-end and upper-end segments behave differently. These prices may have reference to the international London and New York market prices but much of the coffee trade takes place on a price differential basis or outright basis. In the specialty segment, the shares of added value for farmers tend to be much higher than in the mainstream coffee market, though producing and processing specialty coffee requires substantial effort and work.

The Specialty Coffee Association provides an illustrative example of how exporters should look into their value chain, in terms of different costs and margins. You should also refer to the Specialty Coffee Transaction Guide to get an idea of the current market prices for specialty coffee. This guide quantifies anonymous contract and pricing data of importers and roasters, based on quality, quantity, and origin of the coffee purchased.

{kind=link}

Tips:

- Learn more about mainstream Polish supermarkets’, such as Auchan, promoting of standard quality and high-quality coffees. Compare their product assortment and price levels with specialised stores, such as the Polish web shop kawa.pl.

- Check the website of the Specialty Coffee Association (SCA) to learn more about the high-end and upper-end coffee segment, market trends and main players in the whole sector. Refer to the Polish SCA website for more specific information about Poland.

Through what channels can you get coffee on the Polish market?

As an exporter, you can use different channels to bring your coffee to the Polish market. How you enter the market will vary according to the quality of your coffee and your supplying capacity. Bear in mind that shortened supply chains are a general trend in Europe. This means that retailers and coffee roasting companies are increasingly sourcing their green coffee directly from origin.

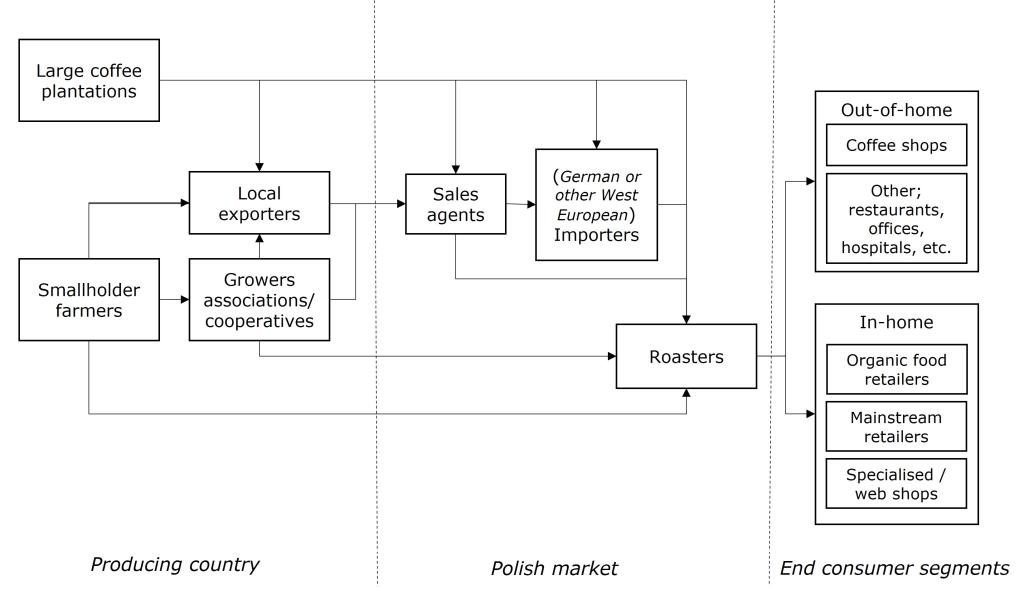

In Poland, the trading structure is different from traditional markets such as Germany, since most Polish importers are not as large and not as actively involved in trading directly from producing countries. However, it is important to also understand the links between Polish roasters and German importers, since Poland sources a large share of its coffee supplies from Germany. The below figure shows the most important market channels for green coffee beans entering Poland.

Figure 5: Market channels for green coffee in Poland

Source: ProFound

Importers

Importers play a vital role in the coffee market, functioning as supply chain managers. They maintain wide portfolios from various origins, pre-finance operations, perform quality control, manage price fluctuations and establish contact between producers and roasters. In most cases, importers have long-standing relationships with their suppliers and customers.

Green coffee beans mainly enter Poland via the Port of Gdynia or Port of Gdańsk. Green coffee traders in Poland are located near these ports. Large-scale importers usually have minimum volume requirements starting at around 10 containers, covering a wide range of qualities, varieties and certifications. At the same time, they provide strong support on logistics, marketing and financial operations.

Bero Polska is the leading supplier of raw, soluble and gourmet coffee in Poland as well as Central and Eastern Europe; it has an office for coffee imports in the city of Gdynia. It belongs to the Neumann Kaffee Gruppe and handles a large range of products, both conventional and specialty coffees. The Olam Group is also present in Poland.

Specialised importers are able to buy small and medium-sized volumes of high-quality and single origin coffees, from micro-lots to full container loads (FCL). These players can also provide marketing expertise, financial support and other green coffee related services, such as logistics, insurance and warehousing. An example of a specialised importer in Poland is Anfrawer.

For which companies is this an interesting entry channel? The most interesting channel for you will depend on the quality of your coffee and your supply capacity in terms of volume. If you are an exporter of green coffee beans and can offer high volumes (10 containers or more), you should look into entering the Polish market through large importing companies. These companies usually have agents or representative offices in producing countries, which can be your first point of contact.

Specialised traders can be interesting if you have evidence of high cupping scores of at least 80, although some buyers may require scores higher than 85, plus a high degree of transparency and traceability. Keep in mind that many specialised importers prefer to work directly with producers or cooperatives.

Large roasters

Most large roasters buy their coffee beans from the country of origin, although they might also source through importers. Roasters usually perform analysis and cup testing to check the evenness of the roast and to identify any defects that can occur in post-harvest processes, such as fermentation, drying and storage. Large roasters usually blend different qualities of green coffees to safeguard quality consistency. The final product is distributed to retailers and the food service industry.

Roasters can operate under their own brands and/or private label. Examples of large roasters operating under their own brands in Poland include Jacobs Douwe Egberts and Tchibo. Examples of private label coffee roasters are René Café and Instanta.

For which companies is this an interesting entry channel? Supplying directly to large-scale roasters is only interesting if you are able to supply large volumes at consistent quality. If you work with bulk coffees, discuss minimum quality and other requirements, such as certification, with your potential buyer.

Small roasters

Although a growing number of small roasters import green coffee directly from the place of origin, the largest share of smaller roasters continues to buy their coffee via importers. This is the case as not all roasters can take on the additional responsibilities and risks involved in importing directly from the source. Importers help roasters with financial services, quality control and logistics. Nevertheless, small roasters often maintain a direct connection with their producers, as they need detailed information for storytelling in order to market the coffee to their clients (brands or consumers). Small roasters often specialise in single origins and the finest specialty coffees.

In the case of Coffee Lab, specialty coffee is selected from the assortments of specialty coffee importers in other European countries such as List and Beisler (Germany) and Belco (France). Examples of small roasters in Poland directly importing coffee include Coffee Proficiency and Blueberry Roasters.

For which companies is this an interesting entry channel? Supplying to small roasters is interesting for producers and exporters that offer high-quality coffees, have micro lots, can guarantee traceability, and are willing to engage in long-term partnerships. Assess whether small or medium-sized roasters are interested in establishing direct trade relationships, and whether you have sufficient means to organise your exports.

Agents

Dealing directly with different green coffee buyers located in several markets is not always feasible. For this reason, many exporters still use agents. Agents act as intermediaries between you, coffee importers and roasters. They have vast market knowledge and know their buyers. Agents can help you assess and select interesting buyers, while they may help buyers find interesting suppliers in different countries. Some agents are independent, while others are hired to make purchases on behalf of a company.

For which company is this an interesting entry channel? If you have limited experience exporting to European countries, agents can be a big help. Agents are also interesting if you have limited quantities of coffee or if you lack the financial and logistical resources to carry out trade activities. Working with an agent is also useful if you need a trusted and reputable partner in the coffee sector. Be prepared to pay them commission for their work.

Tips:

- Find buyers that match your business philosophy and export capacities in terms of quality, volume and certifications. For more tips on finding the right buyer for you, see our study on finding buyers in Europe.

- Attend trade fairs to meet potential Polish buyers. Interesting trade fairs in Europe include SCA’s World of Coffee (every year in a different European city), Biofach (organic) and COTECA (both in Germany), and the Warsaw Coffee Festival. Attending such events can provide you with additional insight into the preferences of Polish buyers with regard to origin, flavour and sustainability certification.

- Check the website of the Specialty Coffee Association Poland and the Warsaw Coffee Festival highlighting several Polish members and exhibitors. It will help you find potential partners and learn more about the Polish market.

- Invest in long-term relationships. Whether you are working through importers or roasters, it is important to establish strategic and sustainable relationships with them. This will help you manage market risks, improve the quality of your product and reach a fair quality-price balance.

- See our study on buyer requirements for coffee to learn about which European market standards and requirements you need to comply with when supplying to Europe.

- See our study on how to do business with European buyers for more information about complying with buyer requirements, how to send samples and how to draw up contracts.

3. What competition do you face on the Polish coffee market?

In general, competition is higher for mainstream coffee with low added value. This segment is mainly dominated by major suppliers and cooperatives which are able to deliver large quantities so they can compete on price. It is difficult for small and medium-sized companies, for example those which only export a few containers per year, to compete in this segment.

Volumes in the specialty coffee market are smaller, and the focus is more on quality, origin and sustainability. However, as the requested volumes are smaller, and more and more producers are focusing on this segment, competition can also be quite fierce. There are several competitions to identify the highest quality coffees produced worldwide, for instance the Cup of Excellence. These competitions might be an interesting entry point for this segment but it may be necessary to invest a large sum of money in order to enter this segment.

New entrants to the market will face competition from already successful coffee exporters, especially due to the fact that they have already established long-term relationships with buyers. Entering the market as a newcomer requires you to have extensive knowledge of your product assortment, stable quality and volumes, and good communication skills to enable you to start building your own new relationships with buyers. If the potential buyer is not yet operating in your country of origin, it might be more difficult to establish initial contact. You may be required to supply more extensive information about the producing regions, the producing communities and traceability, for example.

Brazil is Poland’s largest direct coffee supplier

Brazil is the world’s largest coffee producer and Poland’s second-largest supplier, after Germany. The coffee supplied by Brazil to Poland reached 16 thousand tonnes in 2021, representing a large annual average growth of 47% since 2017. Coffee is one of the top four exports from Brazil to Poland, after copper exports, soybean and raw tobacco. Brazil produces both Arabica (71%) and Robusta (29%) varieties, but about 80% of exports consist of Arabica.

Brazil’s coffee-producing areas are relatively flat, which has intensified the use of mechanical pickers in the industry. This has drastically reduced labour costs in Brazil’s coffee production, but also resulted in lower quality, as machines do not distinguish between ripe and unripe cherries. Coffee prices in Brazil went down, especially in relation to other coffee-producing countries. Brazil mostly produces natural and pulped natural coffees. Low-grade Brazilian Arabica is mostly used in blends.

Although the country is mainly known for exporting large volumes of standard quality coffee, it also has a strong reputation as a producer of specialty coffees. The sector receives considerable institutional support from the Brazil Specialty Coffee Association, which aims to elevate the quality standards and enhance value in the production and marketing of Brazilian coffees. Examples of successful exporters of specialty coffees in Brazil are Burgeon and Bourbon Specialty Coffees. Large Brazilian exporter Costa Café has also started exporting specialty coffees in addition to its regular mainstream coffee exports.

Poland is now a growing market for Brazilian specialty coffee because it is the largest economy in Eastern Europe, it has a large population, and it has a growing specialty coffee sector characterised by the proliferation of high-end coffee shops. Brazilian specialty coffee is expected to continue being promoted on the Polish market thanks to the growing consumption and the popularity of various types and methods of preparation in Poland.

Trade agreements between Vietnam and Poland generate increasing export potential

Vietnam is the world’s second-largest coffee producer, with production volumes reaching 1,740 thousand tonnes by December 2021. Poland imported a total of 11 thousand tonnes of green coffee from Vietnam during 2021. Between 2017 and 2021, imports from Vietnam decreased year on year by 3.5%.

Over 96% of Vietnamese coffee production consisted of Robusta coffees. Vietnam’s coffee production is strongly focused on creating large volumes of standard quality coffees, mostly directed to the instant coffee market. In recent years, Vietnam’s Robusta exports have been faced with fierce competition from the Brazilian Conilon and Robusta beans from other countries, leading to slightly lower export volumes. Examples of large Vietnamese coffee exporter groups include Simexco Daklak, Intimex Group and Mascopex.

It is likely that trade between the European Union and Vietnam will increase again in the near future, as the European Union-Vietnam Free Trade Agreement (EVFTA) entered into force in August 2020. This agreement lifted tariffs on all green, roasted and processed coffee from Vietnam. To help boost coffee trading through the EVFTA, the Vietnamese government asked the country’s coffee industry players to apply advanced cultivation, processing and storage technologies, to better meet the requirements of European importers.

Recently, Vietnam and Poland had bilateral talks to promote two-way agricultural trade cooperation. It is believed that Poland will facilitate the entry of more Vietnamese businesses to Europe, including in the coffee sector.

Uganda’s coffee exports to Poland have been falling steadily

Another major Robusta producer is Uganda. According to USDA’s Coffee: World Markets and Trade report, approximately 84% of total Ugandan green coffee exports is calculated to be Robusta. In 2021, total imports to Poland amounted to over 1.0 thousand tonnes. Between 2017 and 2021, a year-to-year decrease of 20% was registered.

The fact that Uganda is the only African country where green coffee is available throughout the year gives it a strong competitive advantage. However, disruptions in weather and precipitation patterns due to climate change are increasingly leading to supply chain difficulties.

The Uganda Coffee Development Authority (UCDA) helps promote and guide the development of the Ugandan coffee industry through quality assurance, research and improved marketing techniques. UCDA has also encouraged the production and marketing of high-quality Arabica coffees, for instance through the establishment of an online auction to trade specialty coffee since 2018.

Coffee in Uganda is mainly grown by smallholder farmers, who are organised under NUCAFE, the national coffee farmers’ umbrella organisation. NUCAFE’s membership boasts 213 farmer cooperatives and associations. Examples of Ugandan exporters are ACPU and Great Lakes Coffee.

Tanzanian market is recognised for its specialty coffees

In 2021, Tanzania exported more than 1.2 thousand tonnes of green coffee to Poland, which meant a significant growth from the past three years when exports did not exceed 140 tonnes. According to calculations using information from USDA’s Coffee: World Markets and Trade report, Tanzania produces both Arabica (54%) and Robusta (46%) coffee, mainly by smallholder farming households.

Coffee is Tanzania’s largest export crop, but the country is a small coffee supplier to the European market. Tanzanian coffee is mainly traded through a centralised auction system where cooperative societies offer coffee on behalf of farmers. Tanzania Coffee Board (TCB) regulates the coffee industry in Tanzania and advises the government about the growing, processing and marketing of coffee within and outside the country.

For some years now, exporters of specialty coffees can also sell directly but they have to purchase coffee from co-op partners at a higher price than the auction. Tanzania’s Kilimanjaro coffee is internationally renowned for its unique taste and for where it is grown. Also, Tanzania produces a rare specialty coffee called Peaberry that was ranked first among the best coffee beans in the world, demand for which is outstanding.

Examples of Tanzanian exporter companies are Kagera Cooperative Union and Kilimanjaro Native Cooperative Uninon.

Exports of Colombian coffee remain relatively stable

Colombian exports to Poland increased at an average annual rate of 2.0% between 2017 and 2021. During this period, Colombian coffee exports ranged around 540 and 640 tonnes per year, except for 2018 when they recorded a peak of 883 tonnes. Total exports to Poland amounted to 586 tonnes of green coffee in 2021.

Colombia is the world’s largest producer of washed Arabica. By June 2021, Colombia produced 846 thousand tonnes of Arabica coffee. The Colombian Coffee Growers Federation strategically promotes and markets Colombian coffee, solidifying the country’s established image and brand for high-quality coffees. The Café de Colombia trademark is a registered protected geographical indication (PGI) in Europe. Colombia is unique in this regard, as it is the only coffee-producing country to have obtained this designation.

Colombia is an important producer of certified coffees worldwide. Colombia is the second-largest producer of Rainforest Alliance-certified coffees and the largest producer of Fairtrade-certified coffees. The wide availability of certified coffees has allowed green coffee exporters to access various markets and segments in Europe. Examples of successful Colombian cooperatives or private organisations which export coffee to the international market include InConexus, Red Ecolsierra, La Maseta and Cadefihuila.

Decreasing Indian coffee exports to Poland and Europe

India supplied 582 tonnes of green coffee to Poland in 2021. Between 2017 and 2021, green coffee exports decreased by a year-to-year rate of almost 27%, mainly as a result of the need and desire to add value at the coffee processing stages and the COVID-19 pandemic. The Indian coffee industry, which consists mainly of small and medium-scale farmers, is increasingly struggling to keep up with the lower prices offered by Brazilian competitors. Also, excessive rainfall in 2021 caused significant damage to coffee plantations, reducing Indian coffee yields.

An estimated 77% of Indian coffee production is dedicated to Robusta. The largest Indian exporter of Robusta is Olam Agro India.

Indian Robusta is often preferred for blends thanks to its good blending quality. In addition to being known as an interesting Robusta producer, India is also known for its unique Monsoon Malabar coffee, which is exposed to the salty sea air during the monsoon season to acquire a specific taste. The coffee sector in India is promoted by the Coffee Board of India.

Tips:

- Identify your potential competitors. To be successful as an exporter, it is important to learn from them too. Look into their marketing strategies, the product characteristics they highlight and their value addition approaches. Successful companies that already export to the European market from which you can learn include, for example, Bench Maji Coffee (Ethiopia), Aicasa (Peru), and Bourbon Specialty Coffees (Brazil). Another interesting exporting company to learn from is Caravela Coffee, which has a wide portfolio of specialty coffees from Latin America, facilitates contact between roasters and producers, and has set up representative offices in destination markets.

- Identify and promote your unique selling points. Give detailed information about your coffee-growing region or origin, the varieties, qualities, post-harvesting techniques and certification of the coffee you offer. You can also tell the history of your organisation, your coffee growing farm and the passion and dedication of the people working there. These are all elements that make your company unique.

- Actively promote your company on your website and trade fairs. Quality competitions also provide good opportunities to share your story. The auctions organised by the Cup of Excellence are one such example.

- Are you interested in exporting high-quality coffee? Learn more about cupping scores on the website of the Specialty Coffee Association (SCA). You can also consider getting a Q Arabica or Q Robusta Grader certificate to be able to cup and score your coffee through smell and taste according to international standards.

- Work with other coffee producers and exporters in your region if your company size or product volume are too small. As a group, you can promote good-quality coffee from your region and be more attractive and more competitive in the European market.

- Develop long-term partnerships with your buyers, including always complying with their requirements and keeping your promises. This will give you a competitive advantage, more knowledge and stability in the Polish market. See our tips on doing business with European coffee buyers for more information.

ProFound – Advisers In Development carried out this study on behalf of CBI.

Please review our market information disclaimer.

Search

Enter search terms to find market research